Case Study #1 - Am I On Track for Retirement?

This is the first post of a new Case Study series that reviews the financial lives of everyday Canadians. While helping individuals plan and answer pressing questions, we find transferable lessons to help others navigate similar situations. If you have recommendations for future case studies or would like to be featured, please email me. While details were changed to protect the identity of our participants, the information and recommendations are reflective of the situation.

Personal and financial background

Summary

Leon, age 50, lives in Richmond, British Columbia, with his daughter, 18, and son, 15. They rent a three-bedroom townhouse in a housing co-op where they don’t need to worry about property management fees or the risk of being evicted.

Roughly a decade ago, Leon and his wife went through a divorce. At the worst of a financially challenging period, out of necessity, Leon began learning about personal finance. He read books, frequented forums and started to track and manage all of his income, spending and investments. Ten years later, Leon wants to know if his hard work has paid off. He wonders if he’s on track to pay for his children’s post-secondary education and to retire comfortably.

Finances

Assets: Emergency fund of $7,500, car savings of $6,500, RRSP of $120,000, TFSA of $87,000, RESP of $86,000, defined contribution pension plan of $63,000, and other investments outside Canada of $30,000. Total of $400,000.

Liabilities: Personal loan of $27,000.

Income: Leon works in the IT sector and earns a base salary of $110,000 plus a typical annual bonus of $10,000.

Monthly expenses: Rent of $1,245, groceries of $800, child support of $600, transportation of $350, gifts and charity of $320, utilities and maintenance of $315, dining and entertainment of $230, personal expenses of $205, and travel of $200. Total of $4,265.

Review and recommendations

Spending

Leon tracks his spending in Excel and has done an excellent job prioritizing his expenses. He’s identified the essential categories for him and his children (e.g., groceries, travel) and minimized his costs on their non-essentials (e.g., television, meals out). Leon also wanted to keep his housing costs affordable, as this is a significant component of most budgets. He did research to find somewhere that was family-friendly, affordable and stable, and eventually learned about housing co-ops.

Leon’s base income works out to $6,700 a month after-tax. Over the years, Leon has spent time identifying and developing desirable skills to ensure he remains a competitive candidate for well-paying jobs. Leon’s spending allows him to save 36% of his salary for his primary goals of paying for his children’s post-secondary schooling and retirement. He’s also working on topping up his emergency savings to $15,000 and continuing to contribute to his car fund.

Investment planning

Leon manages all of his investments himself. He’s a DIY-er who’s comfortable determining the right amount of risk to take for his goals. To keep his investing low-cost and straightforward, Leon follows a Canadian Couch Potato model portfolio and also uses some of the new all-in-one exchange-traded funds (ETFs).

With 15 years to retirement, his investments are roughly 70% higher-risk (e.g., stocks). As Leon approaches retirement, he plans to use the bucket approach that he learned about through My Own Advisor. With the bucket approach, you invest portions of your portfolio differently depending on when you plan to spend it. The money you’ll need in the next few years is kept risk-free, and cash you don’t expect to spend for ten years or more can be invested more aggressively.

Retirement planning

One of Leon’s primary concerns is whether he’s on track for retirement and if there’s anything else he should be considering.

Leon’s savings and expected income from government pensions [e.g., Canada Pension Plan (CPP), Old Age Security (OAS)] are more than enough to meet his anticipated spending. He’s targeting an annual budget of $55,000 after-tax, increasing each year for inflation. Since Leon moved to Canada later in his career, he should qualify for 75% of the maximum CPP and OAS payments.

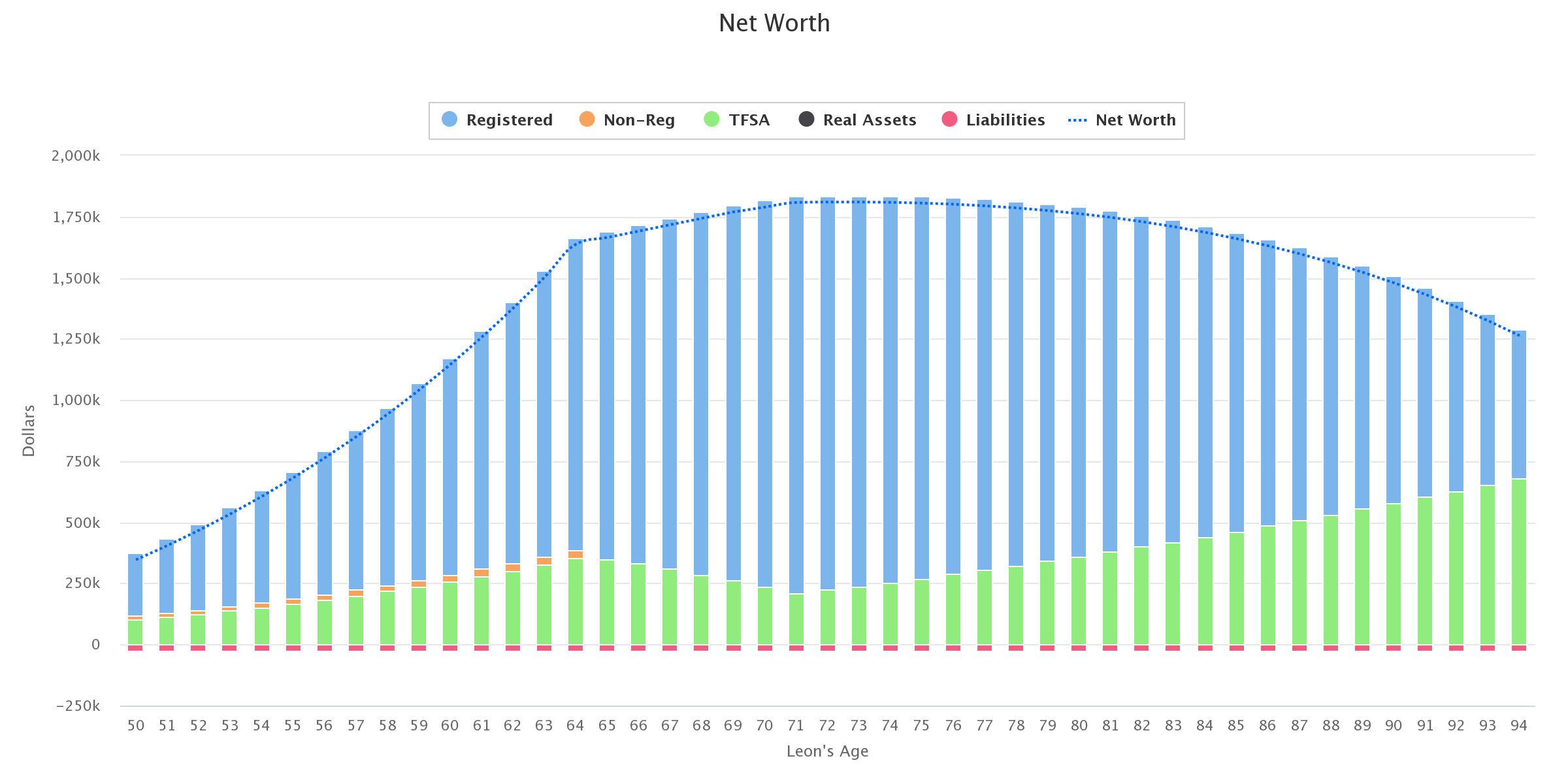

The following chart shows Leon’s annual retirement contributions of roughly $37,000 and existing investments growing to roughly $1.75 million, leading into retirement at 65. Given his current age of 50, Leon has a 25% chance of living to the age of 94 or older.

Source: Snap Projections

The above chart assumes Leon’s income remains stable, and his savings rate continues. If this holds he can explore the following options given his sizable expected surplus:

Save less for retirement and move that to discretionary spending.

Take less risk with his investments.

Retire earlier.

Spend more in retirement.

Gift money to his two children while he’s still living.

Plan for a sizable estate.

Since the future doesn’t always go as planned, we also looked at a scenario where:

Leon loses his job and replaces it with a position earning $80,000.

He changes his retirement target spending from $55,000 to $45,000.

His investment returns are 0.5% lower than expected.

In this case, Leon would begin to run out of savings in his 90s. He’d need to adjust his spending based on his investment returns and health throughout his 70s and 80s.

Source: Snap Projections

An important consideration is that Leon doesn’t yet know how he’ll spend his retirement. He could continue working part-time, volunteer or take up a new hobby. For many Canadians, entering retirement is challenging if you don’t have a plan. Much of your daily routine is now gone, and you can feel lost without goals or a community.

I recommended that Leon consider two or three areas that he wants to prioritize in retirement (e.g., giving back to his community, travelling, spending time with family, learning new hobbies). Once he knows where he’ll focus, this will also help him work towards a more specific retirement budget. MoneySense has a great article from David Hodges titled “Go beyond the numbers of retirement planning” to help consider non-financial retirement needs.

Tax planning

Leon has deposited up to his Tax-Free Savings Account (TFSA) contribution limit and is regularly contributing to his Registered Retirement Savings Plan (RRSP). He’s prioritized the TFSA because of its flexibility.

He receives the Canada child benefit (CCB) for his son and has used the Registered Education Savings Plan (RESP) to help him save for his children’s education. By contributing to the RESP, Leon has received almost $14,000 in government grants that he can use for his children’s post-secondary education.

Risk management (e.g., insurance)

Leon has two life insurance policies:

A term life insurance policy for $200,000 that expires in seven years once both children will have graduated.

A life insurance policy through his employer for an additional $300,000 in coverage.

As the years pass, Leon’s need for insurance coverage will reduce since he’ll have earned more money and covered more of his children’s expenses. By lowering his insurance coverage over time, Leon pays less in premium fees while ensuring his family is looked after.

Estate planning

Leon has a will and power of attorney (for health and financial matters) in place that he plans to update once both his children are 19, the age of majority in BC.

Summary

Leon is in a great spot! After a challenging financial period, out of necessity, Leon took control of his finances and hasn’t looked back. He’s automated as much of his saving and investing as possible to keep things simple and remove himself from day to day decisions. While Leon acknowledges the important role his high income plays in his financial success, his habits and living below his means are also critical.

Transferable lessons

In each Case Study, we find transferable lessons to help you, a friend or a family member. Leon’s case helps us see:

The importance of helping others to learn about personal finance.

Leon provides a great example of what happens once you start learning more about your money. What began out of necessity has turned into a personal passion, and Leon is keen to share his new knowledge with his son and daughter. He’s asked them to each complete two book reviews of a personal finance or personal development book each year.

You haven’t missed the boat. You can start learning at any time.

In just over a decade, Leon built up over $200,000 for his family’s future. While starting early helps, you can be just as successful starting later in life if you build your knowledge base and find the motivation. If you know what you need to do and develop steady habits, you’ll be amazed at how quickly you’ll progress.

Closing remarks

Learning more about your money gives you the flexibility to live the life you want. If you’re looking to learn more, three resources on the site include:

A three-part series on where to start with your money:

The Snowman’s Guide to Personal Finance: A simple approach to managing your money

Thank you to Leon for sharing his experience. If you have recommendations for future case studies or would like to be featured, please email me. If you enjoyed this case study, please consider subscribing to our community at the bottom of the page to receive future emails. If you know someone else who could benefit from the resources on the site, your referral is much appreciated.