TFSA vs. RRSP for Retirement Savings

While I covered this topic in-depth in The Snowman’s Guide to Personal Finance, I wanted to provide a new analogy to help people navigate the question. If you have 20 minutes, I’d encourage you to check out the two chapters that covered the Registered Retirement Savings Plan (RRSP) and Tax-Free Savings Account (TFSA) for a full overview and trade-off discussion. If you’d like a faster read with a simple analogy, please continue below.

Going shopping for investments

As you enter a supermarket, you often face a decision on whether to get a shopping cart or a basket. Your choice will likely depend on:

how long your grocery list is

how quickly you need to get home

how busy the store is, and more

While each serves a slightly different purpose, you often can’t go wrong either way. It’s only in extreme cases, for instance, shopping for a company barbeque or needing to get out of the store in 5 minutes, where there will be a clear winner.

Choosing between a TFSA and RRSP for your retirement savings is surprisingly not much different. Each account allows you to buy the same types of investments to grow your money for the future. However, they’re different enough that one might be better than the other for your needs. Instead of considering your shopping list, you’ll need to consider:

what your current income is

what your future income may be

your preferences, behaviour and more

Summary of the TFSA and RRSP

Both the TFSA and RRSP are accounts that you can open the same way you’d open a chequing or savings account. They both allow you to buy investments (e.g., stocks, bonds, guaranteed investment certificates (GICs), exchange-traded funds (ETFs), mutual funds and more). You don’t pay taxes on any of the profit you make while the money remains in the account. You can only deposit money to either account if you have contribution room available.

Comparing the TFSA and RRSP

The primary differences between the TFSA and RRSP are when and how much you’re taxed. As the following flow chart demonstrates, if you deposit money into a TFSA, you’re taxed on your income today. However, if you deposit money into an RRSP, you don’t pay tax on that income until it’s withdrawn later (often in retirement).

As a result of this difference, the decision of whether to use a TFSA or RRSP often comes down to how much tax you’d pay today vs. how much tax you’d pay in the future.

Comparing tax rates

If your tax rate today is the same as what you would pay in the future, then the TFSA and RRSP are tied for this portion of the comparison. As the below calculations show, whether you pay 20% tax today or in retirement, you’ll end up with the same amount of money. In this case, if you start with $7,000 of your income today, you’ll end up with $18,000 in twenty years. This assumes you earn a 6% return and pay 20% tax today for the TFSA or 20% tax in the future for the RRSP.

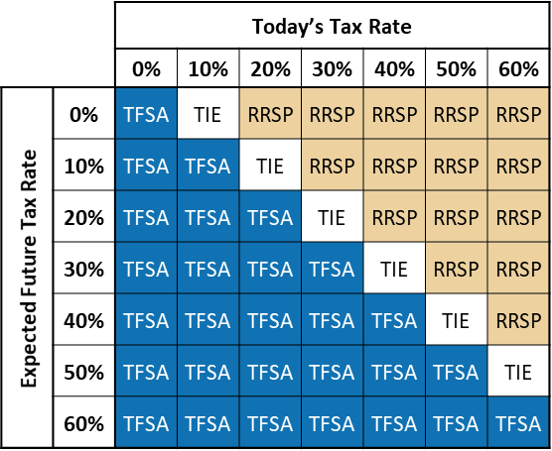

A full comparison across tax rates

The following table outlines that whenever the tax rate you’d pay today is the same as what you’d pay in the future, there’s a tie, and either account will provide the same balance in the end.

If your taxes today are higher than you expect they’ll be in the future, then the RRSP wins, as shown in the top right portion of the table. If, however, you expect your tax rate to increase in the future, the TFSA is preferred.

Additional considerations

While the tax rate is a significant driver, it’s not the only consideration. For people in extreme cases found in the top right corner or bottom left corner, it’s unlikely the following factors will change which account is best for you. However, if you’re on the edge of the ‘tie’ line, as many of us are, then the following topics may impact your decision.

Canada child benefit (CCB) and other income-based government benefits

If you’re currently receiving the CCB or other government benefits that are based on your income level, the RRSP may allow you to increase the benefits you receive. By contributing to an RRSP, you lower your taxable income for the year, increasing the amount the government will provide you in benefits. For example, let’s consider a family with two children earning between $30,450 and $65,976 as a family. If they make an RRSP contribution of $1,000, lowering their taxable income by that amount, they’ll receive an additional $135 in CCB payments.

As a result, if you’re receiving the CCB, this should shift the ‘tie’ line in the above table to the left, making the RRSP preferred in a broader set of cases.

*The shifts to the table we’ll make throughout the remainder of this post are illustrative. The amount you benefit from CCB by making an RRSP contribution depends on your income and number of children.

OAS clawback

Old Age Security (OAS) is a government pension paid to eligible retirees. As of 2020, if you’re receiving OAS payments and earn more than $79,054 income, you need to repay a portion of the OAS to the government. If you expect your income in retirement to be near or above the clawback threshold, then contributing to a TFSA may be preferred. For every $1,000 of income taken out of your RRSP, you need to pay 15% or $150 back to the government for OAS.

As a result, if you expect to receive OAS payments in retirement, and expect your income to be close to the equivalent of $79,000 in today’s dollars, this should shift the ‘tie’ line to the right, making the TFSA preferred in a broader set of cases.

Preference for certainty

One reason the TFSA vs. RRSP discussion is so challenging is that there’s no ‘right’ answer. Because future tax rates and government pension programs are uncertain, even completing all the calculations for your unique case won’t guarantee you make the right choice. As a result, some advantage should be given to the TFSA. Since you’re paying taxes now, and TFSA withdrawals don’t currently impact government pension programs, you’ll have a simpler time planning for retirement with a TFSA.

Self-control

Beyond the math, there are behavioural considerations for how you save for retirement. For some people, the restricted nature of the RRSP (i.e., tax on withdrawals and the loss of contribution room) prevents them from withdrawing money early. However, the tables above depend on you investing your tax refund into your RRSP. If you deposit $5,000 in a TFSA or $5,000 in an RRSP, you’ll be much better off with the TFSA. This is because you don’t have to pay tax in retirement on the TFSA. For the two accounts to be equivalent, you need to contribute your tax refund into the RRSP as well.

US Persons

If you’re a US person, the trade-off may be more straightforward. Since the US doesn’t consider the TFSA to be a tax-exempt account, you’re likely best using an RRSP.

US withholding tax

If you’re investing in US companies, a final and minor consideration is for US withholding tax. When you receive a dividend from a US company in a TFSA, the US government withholds a 15% tax that you don’t receive back. However, since the RRSP was created years ago, the US and Canada have an agreement that the US will not withhold taxes if the dividend is paid to an RRSP. As a result, if you’re investing directly in US stocks or ETFs that pay dividends, you may favour the RRSP all else equal.

Putting it all together for your situation

Using the above tables and additional considerations, you can get a sense of which account is right for you. If you’re still not sure, that’s alright! This is probably because you’re close to the ‘tie’ line. While it may be frustrating not to have a clear answer, it also means you can’t go wrong. The key is to get started as soon as you can. There are several ways you can proceed with your retirement savings:

If there’s a clear winner from the above, open that account type and start setting aside savings.

If there’s no clear winner, you can:

split your contributions between the two account types for the time being.

start with the TFSA and switch to an RRSP later if your situation calls for it.

Closing remarks

Now that you have a sense of which account is right for you, you can learn more about how much you can deposit and other rules from the following posts:

Learn how much you can deposit in a TFSA, as well as just how powerful the tax-free benefit is for your savings goals.

Learn about additional benefits of the RRSP, including the Home Buyers’ Plan (HBP), Lifelong Learning Plan (LLP), as well as how to withdraw from the account as you enter retirement.