Chapter 14: Investment Funds

Stocks and bonds provide the opportunity to grow your money through compounded returns. You could pick and choose individual companies if your interests and skillset permit. Or, a popular alternative is to purchase mutual funds or exchange-traded funds (ETFs). Because it’s challenging to pick the best stock or bond, it can help to own a wide range of investments. This approach maximizes the chance you’ll own a portion of the next breakthrough company.

Mutual funds and ETFs allow you to own a diverse range of shares and bonds with a single purchase. These simple and diversified funds help you benefit from compound growth while minimizing your workload and chance of loss. Rather than having to purchase and manage a long list of stocks and bonds, you can purchase a short list of mutual funds or ETFs. These funds then invest in a diverse range of shares or bonds for you.

Buying a Fund

You can invest in ETFs and mutual funds through most brokerage accounts. You can set up a brokerage account online with a wide range of providers, including most banks. There are differences in the fees you pay, ease of use and speed of transferring money to and from your account. You can find rankings of the top brokerages online. By researching the different companies that offer brokerage accounts, you’ll find the one that’s best for your needs.

You can also invest in mutual funds and ETFs in several other ways. Some options provide advice and help with financial planning, taxes and more. You’ll pay higher fees for these options, but if your situation is more complex or you value the support, it can be worth it. You can also purchase mutual funds directly from the company that manages the fund. Regardless of how you access these funds, they’re an excellent way to simplify investing.

Investment Objective

Each fund has an investment objective that describes what they’ll buy. There are funds that focus on stocks, funds that focus on bonds or those that invest in both. Some funds are split by global markets, such as Canada, U.S., Europe or developing countries. Fixed income funds can focus on corporate bonds or government bonds. They may also invest solely in short- or long-term bonds.

There are many different funds to meet a wide range of investor needs. If you’re saving for two years, you may want a low-risk investment focused on Canadian bonds. In this case, you could buy a fixed income ETF that holds short-term bonds. If you’re saving for retirement, you may invest in four or five different ETFs. This could include:

An ETF that invests in Canadian stocks and bonds

An ETF that invests in U.S. stocks and bonds

A mutual fund that invests in European bonds

An ETF that invests in stocks from developing countries

This demonstrates how you can diversify your investments with just a few funds. It’s important not to invest just in Canada because we’re only a small portion of the global economy.

Management Expense Ratio (MER)

Funds are either actively or passively managed. This difference is important because it often has a large impact on the fees you pay. The management expense ratio (MER) of the fund is one of the most important figures to consider. It’s how much of your money is used on an annual basis to pay for the managing team’s time, resources and expenses. The higher the MER, the more the managers of the fund are costing. Generally, higher MERs—usually greater than 1%—are associated with actively managed funds. These funds do research and regularly buy and sell new investments, experiencing high costs. Less expensive funds—usually with MERs of 0.5% or less—typically follow indexes or broad markets. These funds buy a pre-set list of investments instead of picking and choosing. Therefore, they need less research and trading, thereby lowering their costs.

Exhibit 37 – Funds can be categorized as being actively or passively managed. The approach has a major impact on the fees you pay.

How the MER Impacts Your Return

The MER of a fund is important because it’s a cost that’s independent of the fund’s performance. Therefore, when the fund does well, the MER is deducted before the profits are passed on to you. When the fund does poorly, the MER is still deducted and causes an even larger loss. While 2% may not seem like a significant number, it’s remarkable the impact this fee has on your savings. Another way to consider a 2% MER is to compare it to the total gains that are earned each year. If a fund earns 7% each year, then the fund has spent almost 1/3 of the profits on expenses to operate.

As we saw with companies in Chapter 12, creating value requires you produce something worth more than it costs. Therefore, a fund is only creating value if it can offset the 2% fee with higher returns on the investments it picks. There are various opinions on the benefits of an actively managed portfolio both for and against. So much of the stock market is unpredictable. Therefore, an argument against active management is that the benefits of additional research and speculation don’t offset the costs.

While it may be possible to outperform the market for short periods of time, it’s been very difficult over long periods. There are strong opinions and historical data to support that active management underperforms passive management after considering the higher fees.

An increasingly common approach is to use passive funds that invest in a broad range of companies. Most often, these funds follow an index. The index provides a list of investments determined by a committee or rule set. The goal is to represent a specific market, such as the Canadian or U.S. stock market. An example of an index is the S&P/TSX Composite Index. This is a list of roughly 250 companies that represent approximately 70% of the value of the Canadian stock market.

Another index is the S&P 500. It includes 500 large U.S. companies that are selected by a committee of market professionals. This index is intended to represent the U.S. economy. A fund that follows the S&P 500 can operate at a lower cost than an actively traded fund. This is because the list of companies to invest in is predefined, resulting in less research, trading and other costly activities. Investing in a selection of low MER funds will put more of your money toward earning a return instead of toward fees.

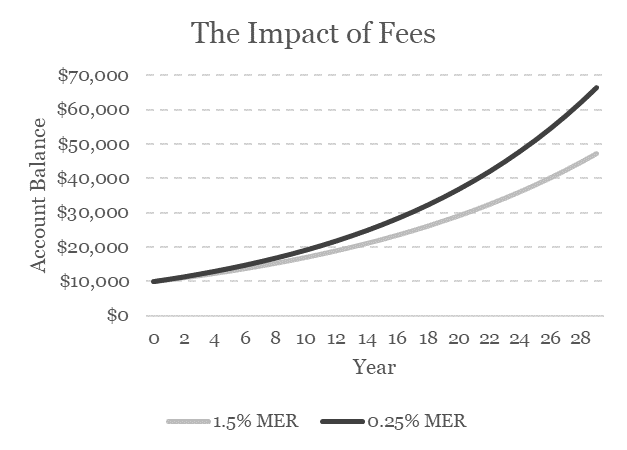

The following example demonstrates how MERs can have a significant impact on the growth of your savings. To achieve this, we’ll compare the result of two savings plans invested in different funds. Both are invested in the Canadian stock market with the same performance of the investments in each fund. The only difference is that one fund will be charged a 1.5% MER, and the second will be charged a 0.25% MER. We’ll assume the Canadian market increases by an average of 7% annually over a thirty-year period.

The first account that is paying 1.5% in fees receives returns of 5.5% a year. This is because the MER is subtracted from the market’s performance. This account will grow from $10,000 to $49,800 over thirty years. The second account that is charged an MER of 0.25% would receive 6.75% growth after fees. The account would, therefore, increase from $10,000 to $71,000. This shows that even though the difference in MER is only 1.25%, the impact to your savings is a loss of 30%. This is because of compound interest, which we discussed in Chapter 2. Once again, this shows that small changes in your rate of return can have a huge impact over long periods of time.

Exhibit 38 – Saving just 1.25% in annual fees allows your account to grow an additional $21,100 over thirty years.

Other Factors to Consider

In addition to reviewing the MER of a given fund, it’s important to consider the track record and any fine print. While historical performance doesn’t guarantee future results, it shows if the fund can meet its investment objectives. Some mutual funds require minimum deposit lengths to avoid additional fees. Other funds have front- or back-end charges to invest in or withdraw money from the fund.

Final Thoughts

Mutual funds and ETFs offer a very simple way to invest. With the purchase of only a few funds, it’s possible to own a diversified set of investments. Stocks and bonds from around the world are available with minimal effort. Mutual funds and ETFs offer the diversification and risk exposure that is so important to the success of your investments. They’re also available without the hassle of purchasing and monitoring numerous individual investments. Through buying funds as you set aside savings, the task of investing for the future is made much easier.

Key Takeaways

ETFs and mutual funds simplify investing by purchasing stocks and bonds for you.

Minimizing the fees you pay will put more of your money to work for your future.

A difference of just 1.25% in annual fees can lower your savings by 30%.

This blog is a duplicate of the recently self-published book The Snowman’s Guide to Personal Finance available for purchase here.