Chapter 10: The Tax-Free Savings Account (TFSA)

Retirement savings are a common and often significant portion of money set aside for the future. However, there are plenty of other reasons you may want to save money. A downside to putting savings in a traditional bank account is that growth earned over time is taxable. This tax can have a significant impact on the speed at which your savings grow. As a result, we’ll discuss another type of account that offers tax advantages and more flexibility than the RRSP.

A Tax-Free Savings Account (TFSA) is a fantastic option when setting aside money for any goal. It can be used for short-term savings toward a car or vacation, medium-term savings for a house or long-term savings to supplement or replace an RRSP in preparing for retirement. It has significantly fewer rules than an RRSP, providing flexibility to meet your needs. The benefit of a TFSA is that any growth on the money held in the account is tax free. This allows for much faster growth of your savings relative to holding them in a traditional savings account.

Traditional savings accounts can also be referred to as non-registered accounts. TFSAs, RRSPs and other accounts with tax advantages are registered with the Canadian Government. A traditional savings account without tax benefits isn’t registered and is therefore called a non-registered account.

Exhibit 26 – This graphic demonstrates that a TFSA completely removes tax on growth. Since growth is tax free, your savings compound at a faster rate, resulting in more money for your goals.

The TFSA was introduced in 2009 and is offered to Canadians eighteen years of age or older. The annual contribution limit in 2009 was $5,000, and it has increased over time. This increase is to account for inflation, which we discussed in Chapter 5. As of 2021, the annual contribution limit is $6,000. You begin earning contribution room when you turn eighteen, and any unused room carries forward indefinitely. Therefore, anyone born in 1991 or earlier who hasn’t deposited to a TFSA has $75,500 in contribution room as of January 1, 2021.

TFSA Benefits

A TFSA is more flexible than an RRSP. For one, withdrawals from a TFSA aren’t taxed. In addition, the amount you withdraw is added back to your contribution room the following calendar year. For instance, if you have $30,000 in a TFSA and withdraw $4,500, you can do so with no penalties or taxes. The following calendar year, you receive the $4,500 back as available contribution room, in addition to the new yearly limit.

The remarkable benefit of the TFSA is that growth on investments in the account are free of tax. This benefit was mentioned in the previous exhibit and the magnitude of the benefit is described through the following two examples. Growth on your investments is normally taxed if held in a traditional savings account. The amount of taxes you’re required to pay depends on the type of growth and your income, which we’ll cover in Chapter 17. The benefit of the TFSA is that you don’t need to worry about those factors since there’s no tax.

To demonstrate just how valuable this is, let’s consider $20,000 in a traditional bank account earning 2% interest. The first year, the account earns $400 in interest, which is taxed just like your regular income. In any given year, the taxes may seem small. However, as we saw in Chapter 2, a small change to your compound growth rate has a significant impact on the end value of your savings. This is especially true over long periods of time.

Let’s continue the process of earning interest and paying taxes—assuming a tax rate of 30%—on that interest for thirty years. With annual tax on the interest, the $20,000 grows to a value of $30,350. Now, if the $20,000 were placed in a TFSA, where it can grow tax free, the account would grow to $36,230.

Exhibit 27 – We’ll use the flow from Exhibit 26 and focus on how much is deposited and how much is withdrawn in each case.

To compare the difference in growth between the two accounts, we’ll subtract the initial $20,000 from the ending balances. With the traditional account, a total of $10,350 is earned, and with a TFSA, $16,230 is earned. In the simplest of comparisons, assuming a low rate of return and a reasonable tax bracket, the TFSA results in 50% more growth. From this, it’s clear the TFSA offers significant value. However, if you’re not yet convinced, the next example will assume a higher return through investing in the stock market.

For simplicity, the following example includes the purchase of the same bundle of stocks in both a traditional account and in a TFSA. Once again, we’ll begin with a $20,000 deposit. This time, we’ll deposit in a brokerage account—a standard account used for investing in stocks, bonds and exchange-traded funds—to purchase the stocks.

After thirty years, at an average annual growth rate of 7%, the initial deposit of $20,000 grows to $152,250. The growth of $132,250 is considered a capital gain. With the current tax system in Canada, half of the gain is added to your yearly income and taxed as usual. Assuming a tax rate of 30%, a total of $19,840 would be owed in taxes. If this same investment were made in a TFSA, there would be no taxes charged. Therefore, you’d have an additional $19,840 toward your goal.

Over-Contributing

It’s important to keep track of your contribution limit for the TFSA to avoid depositing more than you’re allowed. While it would be nice to deposit all your savings in a TFSA, the taxes we pay provide a great deal of good for our country. There’s a constant balance being struck with accounts like the RRSP and TFSA between incenting people to save and collecting a regular stream of taxes. To manage this balance, there’s a penalty if you over-contribute to your account, whether by accident or not. The current penalty for over-contributing is 1% of the overage per calendar month. If your contribution limit is $20,000 and you contribute $21,000, then you’d owe $10 a month until the error is corrected.

TFSA vs. RRSP

We’ve now covered two savings accounts that can assist with long-term savings for retirement. Both the RRSP and TFSA are very helpful in maximizing your personal wealth. The question that may now arise is which account is better to use. The exact answer to this question requires information on your personal circumstances, some speculation about the future and a bit of calculation. While an exact answer isn’t possible on a general basis, there are several factors that can give you a good sense of which account is right for you.

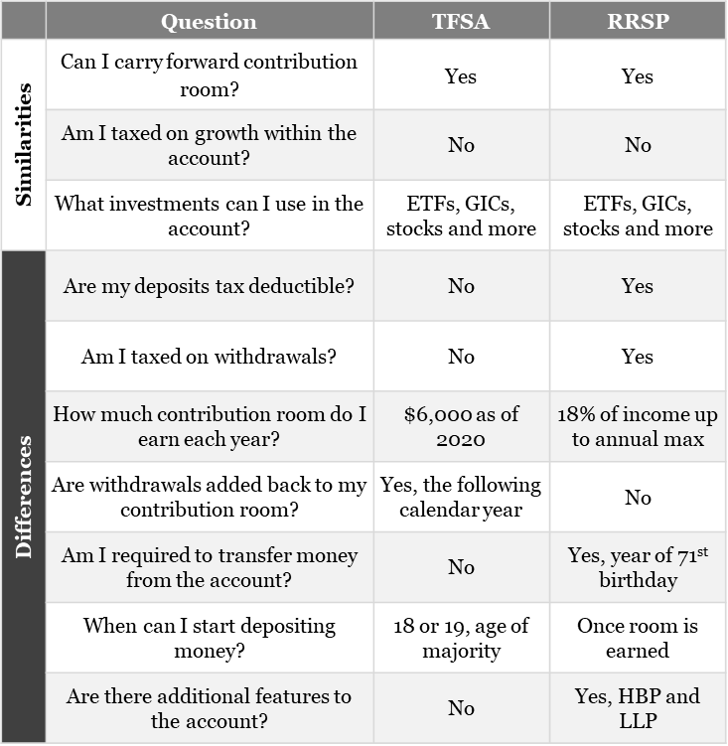

Exhibit 28 – The following table summarizes the main similarities and differences between a TFSA and an RRSP. Withdrawals in the table don’t include the HBP or LLP, which follow different rules that were discussed previously.

Differences: When You Pay Income Tax

We’ll begin by outlining the main difference between the TFSA and the RRSP. A TFSA requires you to pay taxes on your income before you can deposit your money. An RRSP allows you to deposit money before you’ve paid income tax, but it requires you pay taxes when you withdraw.

Exhibit 29 – We can see that the key difference is whether you’re taxed before the deposit is made or after the money is withdrawn.

If you expect a lower tax rate in retirement than you’d pay today, then the advantage goes to the RRSP. For instance, you may receive a tax rebate for 30% of your deposit to an RRSP and only pay 20% tax when you withdraw. In this case, you’d have more than 10% additional money for retirement by using an RRSP.

Exhibit 30 – The below flow shows the above case if you set aside $7,000 of income and earn 6% growth for twenty years.

With the RRSP and a lower tax rate in retirement, you’d have $18,000 rather than $15,700 with the TFSA. However, since tax rates have varied throughout history, there’s no guarantee what you’ll pay in retirement. With that in mind, favouring a TFSA will provide a more certain amount for retirement spending. You won’t be dependent on future tax rates because you’ll have paid everything up front.

Differences: Accessibility of Your Money

The second consideration is how accessible your money is in each account. As we’ve seen, a TFSA allows you to withdraw money at any time with no penalties or taxes. You can even redeposit immediately after if you have the contribution room available. If not, you’ll be able to redeposit in any future calendar year. An RRSP, on the other hand, has a much more restrictive set of withdrawal rules. Whether restrictions to withdrawals are a good or bad thing is dependent on you. If you can resist the temptation to spend money in a TFSA until you’ve reached your goal, then the flexibility is great. However, if you’d prefer to know your money is harder to spend, then the RRSP has the advantage.

Differences: Other Considerations

Several other considerations include taking advantage of the HBP or LLP or figuring out how your income in retirement could impact government pension payments. Certain pension income is provided to lower-income retirees. If you have high income in retirement due to withdrawals from an RRSP or RRIF, you may receive less from the government.

The general theme is that a TFSA provides the greatest flexibility and certainty of what you’ll have in retirement. Meanwhile, the RRSP offers several unique features that can increase the amount you’ll have in certain cases. One approach is to start with a TFSA. Over time, if your circumstances call for it—if you find you’re paying a high tax rate or could use the HBP or LLP—you can withdraw money from your TFSA and transfer it to an RRSP.

Final Thoughts

Regardless of which account you start with, if you reach your contribution limit, the next step is to switch your attention to the other account. If you find yourself in this situation, you’ve done a tremendous job setting yourself up for a great retirement. Steady contributions to a TFSA and/or an RRSP will help you reach your savings goals. It will also ensure the hard work you’re putting in to earn your income today will pay off well into the future. Adding these accounts to your financial plan is like adding a pair of twigs and a black top hat to a snowman.

Key Takeaways

Reduce your taxes and have more money for any goal using your TFSA.

Start with a TFSA for retirement savings until you’ve determined if an RRSP is right for your needs.

Monitor your contribution limit to avoid paying unnecessary fees.

This blog is a duplicate of the recently self-published book The Snowman’s Guide to Personal Finance available for purchase here.