Chapter 9: The Registered Retirement Savings Plan (RRSP)

One of the most important goals people have is being financially stable in retirement. To achieve this, you could deposit your savings in a traditional bank account, like you would if saving for a new TV. Or you could take advantage of specialized savings accounts designed for people saving for retirement. With these specialized accounts, your money will grow faster and larger.

An account that’s specifically designed to help you save for retirement is the Registered Retirement Savings Plan (RRSP). The Canadian Government recognizes the importance of retirement savings for a country’s well-being. Therefore, they offer a series of incentives to encourage you to plan and save for the future. The RRSP is a tremendous option for retirement savings because you can postpone paying taxes until you withdraw.

In addition to the tax benefits, there are several features that make the RRSP versatile for other savings goals. The Home Buyers’ Plan (HBP) and Lifelong Learning Plan (LLP) allow you to use your savings temporarily for other purposes. We’ll cover these features in greater detail shortly, but first, let’s discuss the tax benefits of the RRSP.

Postponing Taxes

The benefit of postponing taxes through an RRSP is best demonstrated by breaking it up into its two components:

You don’t pay income tax on money deposited to an RRSP until it’s withdrawn, most often in retirement.

Your money grows tax free while in the account.

Most people earn a higher income while saving for retirement than they do in retirement. As a result, the taxes you’d pay on income today may be higher than the tax you’ll pay if you wait until retirement. The tax benefit of postponing your income is an instant return on your savings. In addition, because your savings grow tax free while in the account, your balance will increase faster than with a traditional savings account.

Exhibit 23 – The RRSP’s main benefit comes from postponing income taxes and taxes on growth until the money is withdrawn. The below comparison demonstrates how it differs from a traditional savings account.

Postponing Income Tax

Deposits made to your RRSP account can be used to reduce your income. Lowering your income then reduces the amount of taxes you owe to the government. This often results in a tax refund because you’ve likely payed taxes throughout the year on your full income. The value of the refund depends on how much you deposit to the RRSP and your income tax rate. The higher the income tax rate, the higher the benefit of the RRSP.

Take, for instance, Emma, who deposits $2,000 to her RRSP. Since the $2,000 can be deducted from her income, she’d receive a refund for taxes already paid. If the tax rate charged on the $2,000 was 35%, then she’d receive a refund of $700. This results in a deposit of $2,000 into the RRSP that has technically only cost Emma $1,300. If she hadn’t deposited the $2,000 into her RRSP, she’d have paid taxes on it and would only have $1,300 left.

The government helps establish your RRSP now, knowing the money will be taxed when withdrawn. As we mentioned before, the tax rate charged when the money is withdrawn may be lower than what would have been paid today. In Emma’s case, she now has $2,000 in her account that cost her $1,300. If in retirement she’s charged 25% in taxes on the withdrawal, she’d be left with $1,500. Therefore, the equivalent of $1,300 without an RRSP has turned into $1,500 with the account. This potential difference in tax rates between today and retirement allows you to save more money by using an RRSP.

Tax-Free Growth

The second way you postpone tax is because growth in an RRSP account isn’t taxed until the money is withdrawn. Therefore, instead of your savings being taxed yearly, resulting in slower growth, the money grows tax free until it’s needed in retirement.

To demonstrate just how beneficial tax-free growth is, let’s revisit Emma’s case and consider growth on her deposit. Remembering back to the $2,000 contribution, what resulted was a cost of $1,300 to Emma and $700 that came from the government in the way of a tax refund. This means that of the $2,000 currently in the account, $700—or 35%—can be considered from the government.

This idea of distinguishing between the cost of the contribution and the government’s refund is not a common practice. I’m using these labels to illustrate how money flows through an RRSP to properly demonstrate the total value of the account. The full balance of an RRSP is considered the account holder’s money. They’re required to pay taxes only when a withdrawal is made. I’m using the term “the government’s portion” purely to help understand why RRSPs are so valuable.

In our case above, 65% of the account came from Emma and 35% came from the government. The RRSP account begins with an initial value of $2,000. If the savings grew at 7% a year for thirty years, the balance would reach $15,225. Paying 25% in taxes would result in a balance of $11,418.

Now let’s consider if the $1,300, which was Emma’s share of the deposit, grew tax free for thirty years at 7%. The savings would reach $9,896. You’ll notice that you earn more with an RRSP even though you’re paying taxes on your growth when you withdraw. This is because you also get to use the government’s portion of the account.

We can consider the government’s contribution to be the $700 tax refund. This $700 grows in the account for thirty years at 7%. The government’s portion reaches a value of $5,329 by the time retirement arrives. As we saw previously, the tax charged on the withdrawal from the RRSP is only $3,806. This is the 25% tax charged on the total withdrawal of $15,225.

Therefore, when you’re taxed in retirement, provided the tax rate being charged is less than your tax rate when you claimed your contribution, the government isn’t even taking back the taxes they were originally entitled to. In other words, you keep your original cost of $1,300 plus all the gains made on that deposit. As if that wasn’t enough, the government allows you to keep a portion of their share of the growth.

Exhibit 24 – You keep your net contribution, all the growth on it and even some of the growth from the government’s refund. This assumes the tax rate you pay in retirement is lower than your rate when depositing.

Your Income Tax Rates

The most important considerations with an RRSP are the tax rates while you’re depositing the money and when it’s withdrawn. All throughout the previous example, we assumed the rate charged today is higher than the rate in retirement. If this is the case, the benefits of postponing tax through an RRSP are clear. However, if you expect to be charged a higher tax rate in retirement than you are today, then more analysis is required. There’s still the benefit of tax-free growth in the account. But as the tax rate you expect in retirement increases compared to your current rate, the value of the account diminishes.

We’ve now covered the most common and obvious use of the RRSP: to help people save for their retirement. The next two features allow you to use the account for other goals.

The Home Buyers’ Plan (HBP)

The HBP allows you to withdraw from your RRSP to help with the purchase of your first home. To be eligible, you can’t have owned a home within the last five years or have an outstanding balance from a previous HBP. As we discussed in Emma’s case above, let’s consider the government’s tax credit to be their portion of the RRSP. The HBP allows you to borrow the government’s money with no interest expense to buy your home. By depositing money into an RRSP and receiving the tax refund and then withdrawing the money through the HBP, you’ll have more available for your down payment.

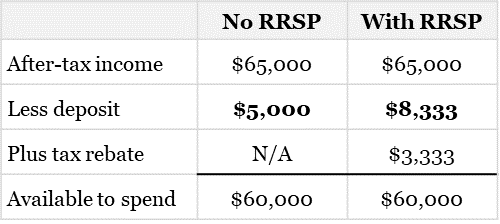

To demonstrate, let’s consider Susan, who plans to purchase a home in three years with savings she’ll start setting aside today. For simplicity, we’ll assume no growth is earned on the savings and focus on the HBP alone. Susan’s net income is $65,000 a year, which results in a marginal tax rate of 40%. The marginal tax rate is the rate of tax she paid on the last dollar she earned, which we’ll learn more about in Chapter 17. Of the $65,000 after-tax income, she needs $60,000 for other savings and living expenses each year. Without an RRSP, Susan places $5,000 a year into a savings account for three years, reaching a balance of $15,000.

However, if Susan used her RRSP, she could collect more money for her down payment. For every $1,000 Susan contributes to her RRSP, she’ll receive a tax refund of $400, since she’s already paid 40% in taxes. Therefore, if Susan contributes $8,333 to her RRSP, she’ll receive a tax refund of $3,333. This leaves Susan with $8,333 in her RRSP and still provides $60,000 for her other needs for the year. If she follows these same steps for the three-year period, she would collect $25,000 in her RRSP. Susan can then withdraw the $25,000 from the RRSP to make the purchase of her new home. The additional $10,000 reduces costs associated with a home purchase, such as mortgage insurance and interest.

Exhibit 25 – By depositing $5,000 into a traditional account or $8,333 to an RRSP, Susan has $60,000 available for her other needs. However, with an RRSP, Susan collects $25,000 over three years for her home purchase instead of $15,000.

HBP Guidelines

In 2019, the maximum withdrawal was increased from $25,000 to $35,000. A contribution must be made to the RRSP ninety days before it’s used for the HBP to still be tax deductible. You receive a two-year grace period after the money is withdrawn before you must start repaying the HBP. After the two years are over, the money must be repaid over the next fifteen years. Each year, you must deposit the outstanding balance divided by the number of years remaining to repay it. For instance, two years after Susan’s $25,000 withdrawal, she must deposit at least $1,667 per year back into her RRSP. Susan could choose to pay it back at a faster rate if desired. Each year, the required deposit is recalculated as the outstanding balance divided by the number of years remaining to pay it back.

If you don’t deposit the required minimum back into your RRSP, there are costs. The difference between the minimum and the amount contributed must be counted as taxable income in that year. If Susan contributes $667 instead of the full $1,667 her first year, she’d need to add $1,000 to her income and pay the required taxes. In addition to paying tax on the $1,000, Susan can’t recontribute this money in the future. Since contribution room to an RRSP is valuable, it’s wise to try and repay at least the minimum amount each year. Any contribution made to repay the HBP is no longer tax deductible since the original contribution that was withdrawn already received that benefit.

The Lifelong Learning Plan (LLP)

The LLP allows you to withdraw from an RRSP to pursue additional schooling. Like the HBP, the major benefit is that you’ll have more money available if you use your RRSP than if you don’t. It’s possible to save on loans by withdrawing temporarily from an RRSP instead. With the LLP, the maximum annual withdrawal is $10,000, with a cumulative maximum of $20,000. There’s typically a grace period of five years from the year of the first withdrawal where repayments aren’t required. After the five-year grace period, you’d have an additional ten years to repay the LLP following similar rules as the HBP.

RRSP Guidelines

We’ve now covered in depth the benefits of contributing to an RRSP. Next, let’s discuss some of the rules and guidelines for depositing. Anyone that has earned contribution room can deposit to an RRSP up until the year of their seventy-first birthday. Each year, you earn 18% of your previous year’s reported income in contribution room. This means with an income of $50,000, you’d earn $9,000 in contribution room. The amount of contribution room is capped by an annual limit that’s determined each year. For reference, in 2018, the maximum contribution room that could be earned was $26,230. This meant anyone with income below $145,722 earned 18% of their income in contribution room. Anyone earning more than $145,722 was capped out by the $26,230 maximum. Any contribution room that is earned and not used each year can be carried forward for future use.

Since unused contribution room is carried forward to future years, you’ll often have a buildup of available room. Whether from summer jobs or other income, you can use this room to start contributing to your RRSP. You can find out what your available contribution room is from the Canada Revenue Agency, which we’ll cover in Chapter 19.

As we’ve mentioned, deposits to your RRSP allow you to lower your income, reducing the taxes you owe. However, you can choose when to lower your income. You can choose to lower your income the same year you make a deposit, or you can wait to lower your income in a future year. It’s rare to wait to lower your income for a future year, but it can help you gain additional tax savings when the right circumstances strike. For instance, if you only work six months out of the year due to school or a sabbatical, your income will be lower for the year. If you have money and contribution room available, you can still deposit to your RRSP and wait to lower your income until a future year. By waiting until the next year when your income and tax rate are likely to be higher, you’ll receive a greater tax benefit.

RRSP Investment Options

We’ve now seen how your savings benefit from being in an RRSP and how to go about depositing your money. Next, we’ll review the investment options available to help your money grow. Stocks, guaranteed investment certificates (GICs), bonds, exchange-traded funds (ETFs) and mutual funds—all of which will be covered shortly—are common investments used in an RRSP.

Depending on the chosen investment option, your required workload and knowledge level will differ. Individual stocks and bonds can be combined in a range of ways to meet most investment needs. However, a higher level of attention and knowledge is often required if you buy them individually. If you’d prefer a simpler approach, then ETFs or mutual funds provide an already bundled option. These funds are managed by experienced professionals and combine stocks and bonds for you. Whether you take a hands-on approach or rely on professionals, the important part is that your investments are growing tax free while in the RRSP.

Registered Retirement Income Fund (RRIF)

After years of saving in an RRSP, the goal is to eventually use the money for your expenses in retirement. To do this, you’ll need to withdraw from the account. Money in an RRSP can be withdrawn or transferred into an RRIF—read as rif—at any point in time. However, it’s most commonly done once you reach retirement. Any withdrawal—aside from special circumstances, such as the HBP and LLP discussed above—made from an RRSP or RRIF is considered taxable income. This means you’ll need to report the withdrawal and pay taxes in the year of the withdrawal. These withdrawals are taxable because you received a tax refund when the initial deposit was made to the RRSP. You postponed paying income taxes when you earned the money and are now required to pay them on the withdrawal.

Often your financial institution will withhold part of the withdrawal and send the money directly to the Canada Revenue Agency. This is like how income tax is withheld and paid on your behalf by your employer. However, the amount withheld by your financial institution often isn’t the total amount you’ll owe. Therefore, it’s important to consider how much tax you’ll eventually owe on any withdrawal from an RRSP or RRIF.

Your RRSP must be closed by December 31 of the year you turn seventy-one. Most often, the money in an RRSP is transferred into a RRIF and gradually withdrawn throughout retirement. However, the money can also be used to purchase an annuity, or it can be withdrawn, likely resulting in significant taxes. Once the RRSP is closed and the money is transferred to a RRIF, no more deposits can be made.

Each year, there’s a minimum withdrawal required from the RRIF. The amount required is calculated based on the value of the account at the start of the year and your age. You can withdraw more than the minimum, but as we mentioned above, these withdrawals are taxable income. Therefore, the more you withdraw in any given year, the higher the tax obligation. Since you’ll likely have income from other sources, it’s worth spending some time each year to determine the most tax efficient approach.

Final Thoughts

Saving for your retirement can feel like a daunting task. With compound growth from investments and the tax advantages of an RRSP, it’s much more manageable. If your current income tax rate is higher than you expect it will be in retirement, then an RRSP is a very useful tool. However, if you expect your income to increase in the years ahead, there’s another account that may be better suited for you. Our next chapter will cover the Tax-Free Savings Account (TFSA). This account provides another great option to help you save for retirement. We’ll provide a list of similarities and differences between the RRSP and TFSA to help you decide which is right for you.

Key Takeaways

Postpone paying higher income taxes today by depositing money to an RRSP.

Invest in any of a broad range of options to grow your money tax free while in the account.

Manage your withdrawals from an RRSP or RRIF to avoid paying excess taxes.

This blog is a duplicate of the recently self-published book The Snowman’s Guide to Personal Finance available for purchase here.